For most people, the hardest part about buying a home (especially the first one) is saving for the down payment. Many people will not have 20% of the purchase price saved for a down payment. With mortgage loan insurance you can put as little as 5% as a down payment.

Mortgage loan insurance protects the lender from default; most Canadian lending institutions are required by law to have it. If the borrower defaults (fails to pay) on the mortgage, the lender is reimbursed by the insurer. The cost for this coverage is in the form of an insurance premium which is often added to the mortgage, or you can choose to pay in a single lump sum at the time of closing. Canada Mortgage and Housing Corporation (CMHC), Sagen and Canada Guarantee are three major providers of this type of insurance in Canada.

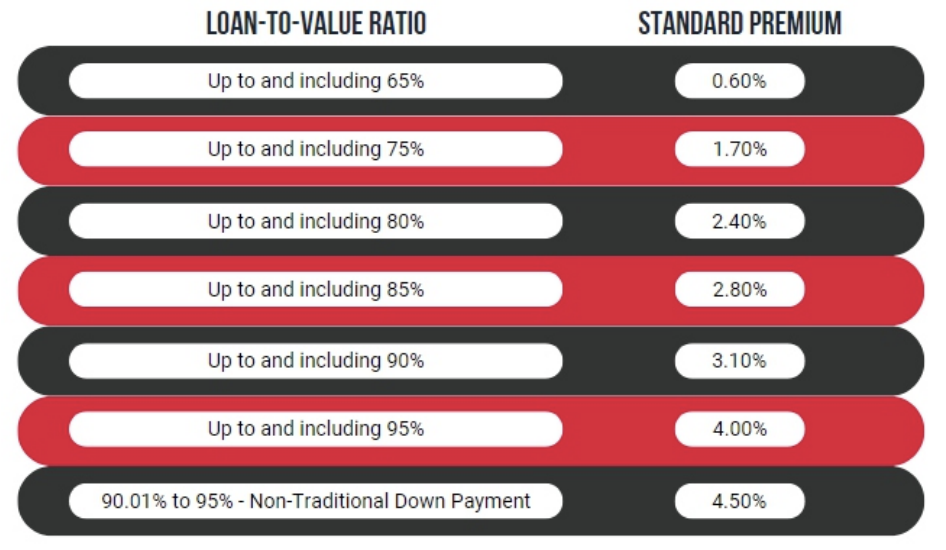

CMHC premiums are as follows:

Minimum Down Payment: Homes Over $500,000

This applies to home buyers who have a down payment of less than 20% and thus require mortgage default insurance. The minimum down payment is 10% for the portion of a house price that exceeds $500,000.

Example:

To break this down, the minimum down payment for a $600,000 home would be $35,000. That's 5% on the first $500,000 ($25,000) and 10% on the next $100,000 ($10,000) in price. That would be a blended down payment of 5.8%.

The trademarks REALTOR®, REALTORS®, and the REALTOR® logo are controlled by The Canadian Real Estate Association (CREA) and identify real estate professionals who are member’s of CREA. The trademarks MLS®, Multiple Listing Service® and the associated logos are owned by CREA and identify the quality of services provided by real estate professionals who are members of CREA. Used under license.

The trademarks REALTOR®, REALTORS®, and the REALTOR® logo are controlled by The Canadian Real Estate Association (CREA) and identify real estate professionals who are member’s of CREA. The trademarks MLS®, Multiple Listing Service® and the associated logos are owned by CREA and identify the quality of services provided by real estate professionals who are members of CREA. Used under license.