Posted on

October 6, 2023

by

Lei Guo

Ottawa MLS® Home Sales Hold Steady in Lackluster September

The number of homes sold through the MLS® System of the Ottawa Real Estate Board (OREB) totaled 946 units in September 2023. This was unchanged from September 2022.

Home sales were 29.6% below the five-year average and 23.6% below the 10-year average for the month of September.

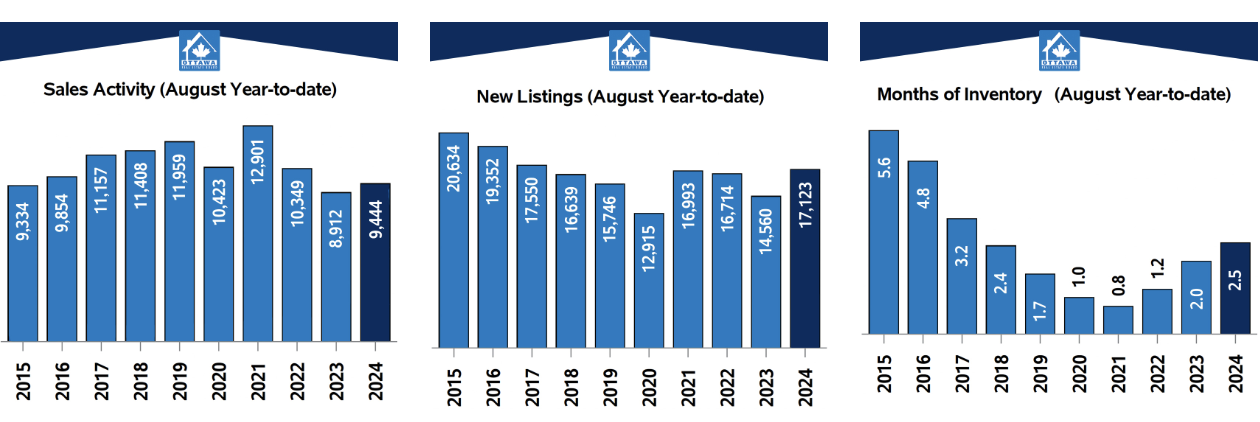

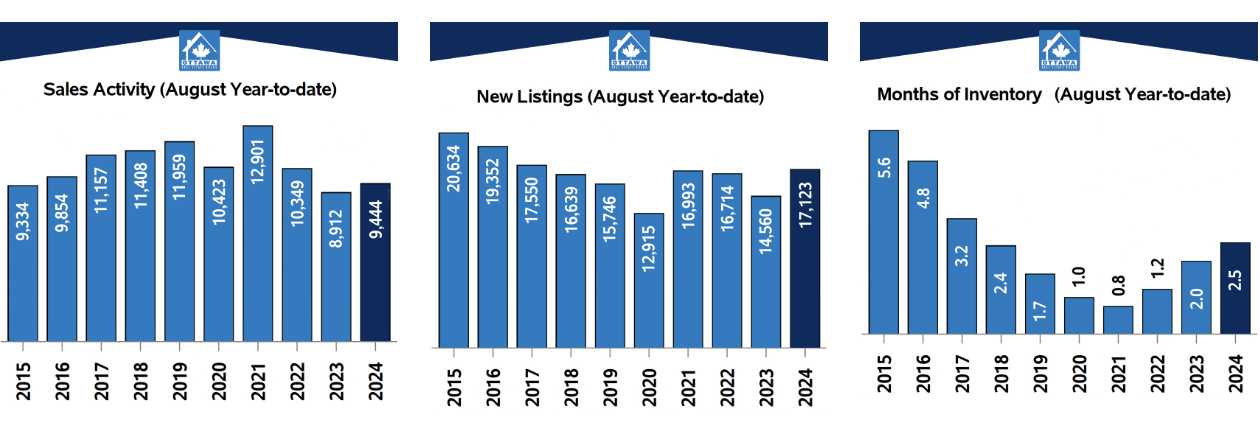

On a year-to-date basis, home sales totaled 9,889 units over the first nine months of the year. This was a large decline of 13% from the same period in 2022.

“Sales activity came in right on par with where it stood at the same time last year but was still running well below typical levels for a September,” said Ken Dekker, OREB President. “New listings have surged in the past several months, which has caused overall inventories to begin gradually rising again. However, available supply is still low by historical standards, and we have ample room to absorb more listings coming on the market. Our market is also right in the middle of balanced territory, and while MLS® Benchmark prices are down from last year they are still trending at about the same levels from 2021.”

By the Numbers – Prices:

The MLS® Home Price Index (HPI) tracks price trends far more accurately than is possible using average or median price measures.

The overall MLS® HPI composite benchmark price was $643,600 in September 2023, nearly unchanged, up only 0.5% compared to September 2022.

The benchmark price for single-family homes was $727,500, essentially unchanged, up just 0.6% on a year-over-year basis in September.

By comparison, the benchmark price for townhouse/row units was $510,900, a small gain of 2.5% compared to a year earlier, while the benchmark apartment price was $422,300, falling by 1.1% from year-ago levels.

The average price of homes sold in September 2023 was $675,412, increasing by 2.7% from September 2022. The more comprehensive year-to-date average price was $672,837, a decline of 6.5% from the first nine months of 2022.

The dollar value of all home sales in September 2023 was $638.9 million, up modestly by 2.7% from the same month in 2022.

OREB cautions that the average sale price can be useful in establishing trends over time but should not be used as an indicator that specific properties have increased or decreased in value. The calculation of the average sale price is based on the total dollar volume of all properties sold. Price will vary from neighbourhood to neighbourhood.

By the Numbers – Inventory & New Listings

The number of new listings saw an increase of 9.8% from September 2022. There were 2,259 new residential listings in September 2023. New listings were 4.8% above the five-year average and 7% above the 10-year average for the month of September.

Active residential listings numbered 2,997 units on the market at the end of September, a sizable gain of 14% from the end of September 2022. Active listings haven’t been this high in the month of September in five years.

Active listings were 33.9% above the five-year average and 18.5% below the 10-year average for the month of September.

Months of inventory numbered 3.2 at the end of September 2023, up from the 2.8 months recorded at the end of September 2022 and below the long-run average of 3.3 months for this time of year. The number of months of inventory is the number of months it would take to sell current inventories at the current rate of sales activity.

Canadians buying homes with family, friends to combat housing affordability woes: Royal LePage survey

According to a recent Royal LePage survey conducted by Leger, six per cent of Canadian homeowners co- own their property with another party, not including their spouse or significant other. Of this group, 89 per cent co-own with family members and seven per cent with friends. Another eight per cent co-own with someone who is not a friend or family member.

Concerning their co-owning situation, 44 per cent of co-owners say that they and all fellow co-owners live in the home together. A smaller percentage (28%) say that they co-own a home with another person(s), but they do not cohabitate. Six per cent of respondents say that they co-own a home with another person(s) and neither party uses the home as a primary residence, rather as an investment or recreational property.

The COVID-19 pandemic forced some Canadians to reconsider their living situation, with many choosing to share living space with friends or family in a time of isolation.

“Different generations of families living under one roof is not a new phenomenon, but has been growing in popularity in recent years,” said Karen Yolevski, COO, Royal LePage Real Estate Services Ltd. “Census data shows that multigenerational households are now the fastest growing household type in Canada. Households group together for many reasons, including communal care for elderly parents, help raising children, cultural preferences or simply to be together.

However, the decision to live together, including co-owning a home, is a decision increasingly made for financial reasons. In an environment where home prices and interest rates have risen quickly and sharply, and where the threshold to qualify for a mortgage has become much more challenging, Canadians are pooling their resources and buying homes together. In cases where homebuyers cannot afford to purchase on their own, they are combining their buying power with their parents, children, siblings or even friends.” “In a market beset by reduced home supply, escalating prices, tightened mortgage qualification requirements, and the highest borrowing rates in more than two decades, many buyers are having difficulties securing the property that they want. Some Canadians are using co-ownership as a way of boosting their borrowing capacity or lowering their monthly mortgage costs, helping them achieve their goal of home ownership,” said Yolevski. “By dividing the cost of a home between more people, Canadians can not only get their foot on the property ladder more easily, but also expand their home search to more desirable locations or larger properties that may not have been accessible with their budget alone.”

Of those who co-own a home with another person(s) and live in the home together, nearly half (49%) say that they purchased the home with another party because they would not have been able to afford a home on their own. Thirty-eight per cent say that by co-owning, they were able to afford a larger property and/or a property in a more desirable neighbourhood. Thirty per cent say that they purchased a co-owned home because they required family support with childcare or taking care of elderly relatives.

“Opting to co-own with friends or family is not as simple as signing a piece of paper next to someone else's name – co-owning a home often comes with meaningful lifestyle changes, and requires in-depth conversations over financial, legal and personal obligations,” said Yolevski. “Regardless of whether you live in the home with your fellow co-owners or not, the responsibilities of owning a home with other people are shared, but so are the benefits.”

The trademarks REALTOR®, REALTORS®, and the REALTOR® logo are controlled by The Canadian Real Estate Association (CREA) and identify real estate professionals who are member’s of CREA. The trademarks MLS®, Multiple Listing Service® and the associated logos are owned by CREA and identify the quality of services provided by real estate professionals who are members of CREA. Used under license.

The trademarks REALTOR®, REALTORS®, and the REALTOR® logo are controlled by The Canadian Real Estate Association (CREA) and identify real estate professionals who are member’s of CREA. The trademarks MLS®, Multiple Listing Service® and the associated logos are owned by CREA and identify the quality of services provided by real estate professionals who are members of CREA. Used under license.